In the world of entrepreneurship, choosing the right legal structure for your business can significantly impact your operations, tax implications, and growth potential. Among the various business entities, S-Corporations are often a go-to option for their unique blend of advantages, but they’re not without their challenges. Our exploration dives deep into the complexities of S-Corporation ownership, spotlighting the key benefits and hurdles that come with this choice.

Contents

Defining S-Corporation

Before we jump into the advantages and disadvantages of S-Corporation ownership, it’s essential to understand what an S-Corporation is, its origins, and how it differentiates from other types of business entities.

History of S-Corporations

The S-Corporation originated in the United States during the mid-20th century. With the Revenue Act of 1958, the U.S. Congress created this business entity as a means of encouraging and supporting the growth of small and family businesses. The ‘S’ in S-Corporation comes from Subchapter S of Chapter 1 of the Internal Revenue Code, where it is described in detail. Over the years, S-Corporations have remained a popular choice among entrepreneurs due to their unique blend of benefits.

Basic Definition and Unique Features

An S-Corporation, in its simplest terms, is a corporation that elects to pass its corporate income, credits, deductions, and losses through to its shareholders for federal tax purposes. This allows S-Corporations to avoid double taxation on corporate income – a significant advantage that we’ll discuss later in this post.

While it may share several features with a standard corporation (also known as a C-Corporation), an S-Corporation possesses unique attributes. For instance, all shareholders must be U.S. citizens or residents, and there is a limit of 100 shareholders. Additionally, S-Corporations can only have one class of stock [1].

How S-Corporation Differs from Other Business Entities

When compared to other business entities, S-Corporations stand out primarily because of their tax status. Unlike C-Corporations, which pay corporate taxes on profits and shareholders pay taxes on dividends, an S-Corporation’s income or losses are directly passed onto shareholders and are taxed at individual income tax rates. This unique structure makes them a hybrid entity of sorts, blending features of corporations and partnerships.

Moreover, unlike Sole Proprietorships or General Partnerships where owners have unlimited personal liability for business debts, S-Corporations offer limited liability protection. This means shareholders are typically not personally responsible for business debts and liabilities.

Advantages of S-Corporation Ownership

Now that we have a solid understanding of what an S-Corporation is, let’s shift our focus to the benefits that it offers. While S-Corporations provide several advantages, we’ll spotlight the key perks: pass-through taxation, limited liability protection, ease of transfer of ownership, and appeal to investors.

Pass-Through Taxation

A core advantage of an S-Corporation is its special tax status known as pass-through taxation. But what exactly does this mean, and why is it beneficial?

Explanation and Benefits

Pass-through taxation refers to the process where the corporation’s income, deductions, and losses are passed directly to the shareholders’ individual tax returns, avoiding the double taxation that occurs with C-Corporations. This means that corporate profits are taxed just once at the individual tax rate, instead of being taxed at the corporate level first and then at the individual level upon distribution as dividends.

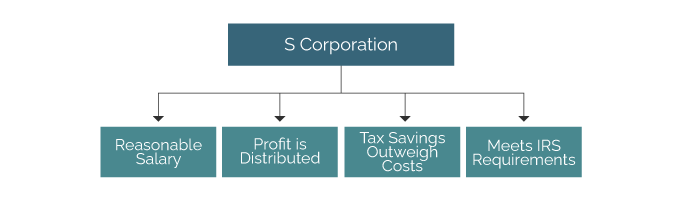

This approach can potentially lead to significant tax savings, especially if individual shareholders fall in a lower tax bracket than the corporation would have.

Real-World Examples

For instance, consider an S-Corporation with a net income of $100,000 for a fiscal year. The corporation does not pay taxes on this income. Instead, the profit is divided among the shareholders who then report it on their individual tax returns. If a shareholder owns 50% of the corporation, they would report $50,000 of income. Depending on their individual tax rate, their tax liability could be substantially lower than what it might have been if the income was taxed at the corporate level.

Limited Liability Protection

Another significant advantage of S-Corporation ownership is the protection it offers against personal liability. Let’s take a closer look.

Explanation and Benefits

Like a C-Corporation, an S-Corporation is a separate legal entity, offering its shareholders limited liability protection. This means that shareholders are not personally liable for the corporation’s debts and liabilities. Their personal assets such as homes, cars, or personal bank accounts are protected in case the corporation faces bankruptcy or lawsuits [2].

Real-World Examples

For example, if an S-Corporation borrows money and cannot repay the loan, the shareholders are not responsible for this debt. The worst-case scenario for shareholders is usually the loss of their investment in the corporation, safeguarding their personal assets from any corporate mishap.

Ease of Transfer of Ownership

One less-discussed but significant advantage of S-Corporations is the relative ease with which ownership can be transferred.

Explanation and Benefits

Ownership in an S-Corporation can be freely transferred without triggering adverse tax consequences—an attribute that does not apply to partnerships and limited liability companies (LLCs). This makes it simpler to sell or transfer ownership of the business, providing flexibility to shareholders.

Real-World Examples

For example, if a shareholder decides to retire or wants to sell their shares for personal reasons, they can do so easily, and the buyer can simply step into their shoes. This ease of transferability can be particularly advantageous in succession planning for family-owned businesses.

Attraction for Investors

Lastly, let’s explore how the structure of an S-Corporation can make it appealing to investors.

Explanation and Benefits

Investors often find S-Corporations attractive because of the pass-through tax status and limited liability protection. It provides an opportunity for investors to directly share in the corporation’s profits while their personal assets remain protected. The ease of transfer of ownership also enhances the liquidity of their investment.

Real-World Examples

Consider a potential investor choosing between investing in an LLC and an S-Corporation. The investor might lean towards the S-Corporation because, unlike an LLC, which can complicate things due to its regulations on profit distribution, an S-Corporation allows for straightforward distribution based on the percentage of ownership [3].

Disadvantages of S-Corporation Ownership

While the advantages of S-Corporation ownership can be enticing, it’s crucial to recognize that there are also drawbacks. As with any business entity, there are certain challenges and restrictions that accompany an S-Corporation structure.

Restrictions on Ownership

One of the key limitations of an S-Corporation is its restrictions on ownership.

Explanation and Drawbacks

S-Corporations can have no more than 100 shareholders, and all shareholders must be individuals who are U.S. citizens or residents. This can limit the potential for expansion and investment. Additionally, S-Corporations are not allowed to have more than one class of stock, limiting flexibility in how profits and losses can be allocated among shareholders.

Real-World Examples

Imagine an S-Corporation that is thriving and wishes to bring in more investors to accelerate its growth. However, it has already reached the 100 shareholder limit. It would not be able to expand its shareholder base unless it changed its corporate structure or one of the current shareholders decided to sell their shares.

Shareholders who are also employees of the S-Corporation are required to receive a reasonable salary, which comes with its own set of drawbacks.

Explanation and Drawbacks

If you’re a shareholder and an employee of your S-Corporation, the IRS requires you to receive a “reasonable compensation” for your services. This salary is subject to federal income tax, Social Security tax, and Medicare tax. The IRS may reclassify corporate earnings as wages if it finds that the S-Corporation is not paying reasonable salaries, resulting in higher tax and penalties.

Real-World Examples

Consider a shareholder-employee who wishes to minimize their salary to reduce employment tax liabilities. They draw a minimal salary and take the rest of their income as dividends from the S-Corporation. If the IRS determines that the salary is not “reasonable” compared to the services provided, it could reclassify the dividends as wages, leading to back taxes and penalties [4].

Potential for Increased IRS Scrutiny

While the pass-through taxation of an S-Corporation is an advantage, it can also lead to increased scrutiny from the IRS.

Explanation and Drawbacks

S-Corporations are more likely to be audited by the IRS compared to other business entities, primarily due to the potential for abuse of the salary requirement for shareholder-employees. This can lead to additional stress, time, and cost to prepare for and manage an audit.

Real-World Examples

An S-Corporation that consistently reports losses or minimal profits while its shareholder-employees receive low salaries but substantial dividends might raise red flags and trigger an IRS audit. In this scenario, the S-Corporation and its shareholders would need to invest time, resources, and potentially legal counsel to handle the audit process.

Complexity and Costs of Formation and Operation

Finally, the formation and operation of an S-Corporation can be complex and costly compared to other business entities.

Explanation and Drawbacks

Starting an S-Corporation involves more paperwork, legal formalities, and costs than establishing a sole proprietorship or partnership. There are also ongoing requirements, such as annual meetings and record-keeping, which can add to the operational complexities. These aspects might discourage some entrepreneurs who prefer a simpler, less formal business structure.

Real-World Examples

For instance, an entrepreneur looking to start a small, locally-focused business might find the process of forming an S-Corporation, such as filing the Articles of Incorporation and creating bylaws, too daunting or time-consuming. They might opt for a simpler business entity, like a sole proprietorship or a partnership, to avoid these complexities.

When to Consider S-Corporation Ownership

Choosing the right business structure is a significant decision and should be made with careful consideration of the unique circumstances and needs of your business. An S-Corporation may be a good fit for you if the advantages align well with your business model and outweigh the disadvantages in your specific context.

Suitable Business Size

The size of your business is an important factor when considering S-Corporation ownership.

Ideal for Small to Medium Enterprises

S-Corporations are typically ideal for small to medium-sized businesses due to the limit on the number of shareholders. If your business plans do not include raising capital from a large number of shareholders or from non-U.S. investors, an S-Corporation might be a suitable choice [5].

Not Ideal for Large Enterprises

However, if you envision your business rapidly expanding with a broad investor base or if you plan on going public in the future, a C-Corporation would likely be a more appropriate choice due to its allowance for unlimited shareholders and multiple classes of stock.

Tax Considerations

The potential tax benefits of an S-Corporation are one of the most compelling reasons to consider this structure.

When Pass-Through Taxation is Beneficial

If your business is profitable and the owners fall in a lower individual tax bracket compared to the corporate tax rate, the pass-through taxation feature of an S-Corporation could result in significant tax savings.

Considerations for High-Income Earning Businesses

On the other hand, if the owners are in a high tax bracket, the benefit of pass-through taxation might be less significant. In such cases, a C-Corporation, which offers the possibility of keeping profits in the company at a potentially lower corporate tax rate, might be more advantageous.

Protection of Personal Assets

The level of risk involved in your business and the need to protect personal assets should also be factored into the decision.

High Risk Businesses

If your business is in an industry with a high level of risk or liability, the limited liability protection offered by an S-Corporation can protect your personal assets from business debts or lawsuits.

Low Risk Businesses

For businesses with a lower risk profile or if the owners have few personal assets to protect, the cost and complexity of forming and operating an S-Corporation might outweigh the benefits of limited liability protection.

References

[1] Compare S corporation vs C corporation

[2] S Corporation Limited Liability Companies: Pick Your Paradigm

[3] S Corporations and ESOPs

[4] S Corporation Shareholders and Taxes

[5] What Is an S Corp?