One of the greatest challenges businesses face is navigating the complex landscape of taxation. For many, the fear of double taxation – where both the corporation’s income and the shareholders’ dividends are taxed – can be a significant hurdle. Enter the S-Corporation, a business structure that offers the unique benefit of avoiding this double taxation.

Contents

Understanding Double Taxation

Before examining the realm of S-Corporations and how they can help avoid double taxation, it’s essential to fully understand what double taxation means. The term double taxation may sound intimidating, and rightly so – it’s a concept that can significantly impact a business’s bottom line.

Explanation of Double Taxation Concept

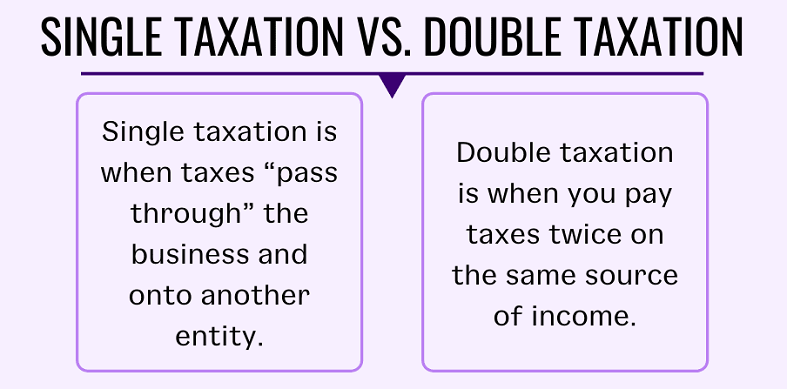

Double taxation occurs when the same income gets taxed twice – first at the corporate level when it’s earned, and then again at the individual level when it’s distributed as dividends. This scenario is common in traditional C-Corporations. In this case, the corporation pays tax on its profits, and then shareholders also pay income tax on any dividends received, which are paid out of these same after-tax profits.

How It Affects Traditional Corporations (C-Corporations)

To give a clearer picture, let’s consider a hypothetical example. Say, for instance, a C-Corporation makes a profit of $100,000. The corporate income tax rate is 21%, so the corporation pays $21,000 in taxes. This leaves $79,000, out of which it distributes $50,000 as dividends to its shareholders. These dividends are then subject to personal income tax. If a shareholder is in the 24% tax bracket, they would pay an additional $12,000 in taxes on the dividends.

Therefore, of the original $100,000 profit, $33,000 (or 33%) has gone to taxes at both the corporate and individual levels, showing how double taxation can eat into profits [1].

Real-Life Examples of Double Taxation

One of the most prominent real-life examples of double taxation is large multinational companies. These companies often face double taxation on their income in different jurisdictions. For instance, if a US-based company operates in Europe, it may have to pay taxes on its income in Europe and then again in the US.

However, it’s not just large corporations that are subject to double taxation. Small and medium-sized businesses structured as C-Corporations also face this issue, making it a significant concern for businesses of all sizes.

Basics of S-Corporation

Having established the concept and implications of double taxation, it’s time to introduce the protagonist of our discussion: the S-Corporation. This business entity offers a way to bypass double taxation and comes with its own set of rules and benefits.

Definition of S-Corporation

An S-Corporation, also known as a Subchapter S Corporation, is a special type of corporation created through an IRS tax election. By choosing to become an S-Corporation, a business can pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes.

Unlike a traditional C-Corporation, an S-Corporation is not subject to federal income tax. Instead, the corporation’s income or losses are divided among and passed through to its shareholders. The shareholders then report this income or loss on their individual tax returns.

Process of Forming an S-Corporation

Forming an S-Corporation involves several steps. First, the business must be eligible to become an S-Corporation. This means it must be a domestic corporation, have only allowable shareholders (including individuals, certain trusts, and estates), have no more than 100 shareholders, have only one class of stock, and not be an ineligible corporation (certain financial institutions, insurance companies, and domestic international sales corporations).

Once eligibility is confirmed, the corporation needs to file Form 2553, “Election by a Small Business Corporation,” with the IRS. This form must be signed by all shareholders and filed within a certain period of time to take effect for the current tax year.

It’s worth noting that some states may require an additional state-level S-election in addition to the federal election. Always consult with a tax advisor or legal expert to ensure you’re meeting all requirements [2].

Ideal Businesses for S-Corporation Status

S-Corporation status can be beneficial for a variety of businesses. Generally, businesses that consistently generate profits and distribute most of these profits to shareholders can benefit the most from an S-Corporation’s tax structure. This is because S-Corporation status allows for income to be passed through to shareholders, rather than being taxed at the corporate level.

However, S-Corporation status is not for everyone. The restrictions on number and type of shareholders, along with the one class of stock limitation, may not suit businesses planning to go public or seeking external investment.

Taxation Structure of S-Corporations

One of the key elements that differentiates an S-Corporation from a traditional C-Corporation is its unique taxation structure. Understanding this structure is vital to grasp how an S-Corporation can help avoid the burden of double taxation.

Pass-Through Taxation: An Explanation

At the heart of an S-Corporation’s taxation structure is the concept of pass-through taxation. This structure allows the corporation’s income, deductions, and credits to pass directly through to the shareholders. The shareholders then report these items on their individual tax returns, and pay tax at their individual income tax rates.

This is a significant departure from the tax structure of a C-Corporation, where the corporation pays corporate income tax on its profits, and then shareholders also pay income tax on any dividends received [3].

How S-Corporations Avoid Double Taxation

By adopting the pass-through taxation structure, S-Corporations effectively eliminate the issue of double taxation. Here’s how: When an S-Corporation makes a profit, that income is passed through to the shareholders. The shareholders then pay tax on this income at their individual income tax rates.

Importantly, this income is not subject to corporate income tax, and the dividends that shareholders receive are not subject to personal income tax. This is because these dividends are paid out of income that has already been accounted for on the shareholders’ personal tax returns.

Comparing Taxation of S-Corporation and C-Corporation

To better understand the benefit, consider a simple comparison between an S-Corporation and a C-Corporation. Suppose both corporations earn $100,000 in profits. In a C-Corporation, the corporation would pay 21% in corporate income tax, leaving $79,000. If the corporation then distributes $50,000 in dividends to its shareholders, those dividends would be subject to personal income tax.

In contrast, in an S-Corporation, the full $100,000 would be passed through to the shareholders, who would then pay tax at their individual tax rates. There would be no additional tax when dividends are distributed.

Benefits of S-Corporation Status

Given the unique taxation structure of S-Corporations, it’s clear that there are potential tax benefits to be gained. However, it’s also important to recognize that the advantages extend beyond just tax considerations.

Detailed Explanation of Tax Benefits

The primary tax benefit of an S-Corporation is the avoidance of double taxation, as discussed earlier. By allowing income and losses to pass through directly to shareholders, S-Corporations bypass the corporate income tax that C-Corporations must pay.

Furthermore, another potential tax advantage pertains to self-employment taxes. In an S-Corporation, only the salary paid to the employee-owner is subject to employment tax. The remaining income that is paid as a distribution is not subject to self-employment tax. Therefore, an S-Corporation can provide a way to minimize self-employment tax liability [4].

Non-Tax Benefits of S-Corporation Status

Beyond the tax advantages, S-Corporations also come with several non-tax benefits.

Limited Liability

Just like C-Corporations, S-Corporations provide their shareholders with limited liability protection. This means that shareholders typically are not personally responsible for the corporation’s debts and liabilities.

Ease of Transfer

S-Corporation interests can be freely transferred without triggering adverse tax consequences – a feature not available in partnerships or Limited Liability Companies (LLCs). This can make it easier for S-Corporations to raise capital and to transfer ownership.

Perpetual Existence

S-Corporations, like other corporations, have an unlimited life span; the corporation continues to exist even if the owner leaves or passes away.

Case Studies Showing Benefits of S-Corporation Status

Several real-world case studies illustrate the benefits of S-Corporation status. For instance, a small business owner who transitions their business from a sole proprietorship to an S-Corporation could potentially save thousands of dollars each year on self-employment taxes alone. Meanwhile, a family-owned business might use S-Corporation status to easily and efficiently transfer ownership between family members.

Tax Planning Strategies for S-Corporations

Choosing to operate as an S-Corporation can certainly offer several benefits, but maximizing these benefits often requires careful tax planning.

Balancing Salary and Dividends

One of the key tax planning strategies for an S-Corporation revolves around the balance between salary and dividends. As mentioned earlier, in an S-Corporation, only the salary paid to the employee-owner is subject to employment tax. The remaining income paid as a distribution is not subject to self-employment tax [5].

Therefore, it might seem advantageous to minimize salary and maximize dividends. However, the IRS requires that shareholders who work as employees receive a “reasonable compensation” for their services before any dividends are paid. If the IRS determines that a shareholder-employee’s salary is artificially low to avoid employment taxes, it may reclassify some dividends as salary, resulting in back taxes, interest, and penalties. Therefore, it’s crucial to strike a reasonable balance between salary and dividends.

Maximizing Deductions

S-Corporations, like other businesses, should also seek to maximize their deductions. Deductions might include business expenses like rent, utilities, office supplies, and business-related travel. Maximizing deductions can help to reduce the overall income that is passed through to shareholders, thereby reducing the total tax liability.

Additionally, under certain conditions, S-Corporation shareholders can deduct their share of the corporation’s losses on their personal tax returns. However, this is subject to limitations based on the shareholder’s basis in the corporation, which is a measure of the shareholder’s investment in the business.

Proactive Year-End Tax Planning

Year-end tax planning is another strategy that can be beneficial for S-Corporations. For instance, an S-Corporation might decide to delay income to the next tax year, or accelerate deductions into the current tax year, in order to minimize the income that gets passed through to shareholders. However, this strategy requires careful planning and knowledge of the tax laws to ensure compliance with IRS rules.

References

[1] S Corporations

[2] How to Avoid Double Taxation as an LLC or S Corporation

[3] How to Avoid Double Taxation with an S Corporation

[4] Understanding S Corporations

[5] Taxes and Corporate Choice of Organizational Form