Understanding and navigating the complex world of taxes is a vital part of running any business, especially when it’s an S-Corporation. Here we make things clearer, particularly when it comes to payroll taxes. We demystify payroll taxes for S-Corporation owners, breaking down the complex tax law jargon into plain English.

Understanding S-Corporations

The concept of an S-Corporation may seem daunting to many. But once you look into the details, it’s not as complex as it first appears.

Definition and Characteristics of an S-Corporation

An S-Corporation, often abbreviated as an S-Corp, is a special type of corporation created through an IRS tax election. By choosing to become an S-Corporation, businesses can pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes.

One key feature of an S-Corporation is its “pass-through” taxation, which means that the corporation itself is not subject to federal income tax. Instead, the company’s income, losses, deductions, and credits are passed through to shareholders, who report this information on their personal tax returns.

Other characteristics include limited liability protection, where shareholders’ personal assets are generally protected from company debts and liabilities. Additionally, S-Corporations can freely transfer stock, but they are subject to certain limitations, including a maximum of 100 shareholders, all of whom must be U.S. citizens or residents.

Comparison of S-Corporation with Other Business Entities

Now that we have a grasp on what an S-Corporation is, it’s essential to understand how it stands out from other business structures.

Unlike a traditional C-Corporation, which is subject to “double taxation” (once at the corporate level and again at the individual level), an S-Corporation is only taxed at the individual level due to its pass-through tax status. This often results in a significant tax advantage for S-Corporations.

Compared to a sole proprietorship or partnership, an S-Corporation offers the advantage of limited liability protection, meaning that shareholders are generally not personally responsible for business debts and liabilities.

However, it’s worth noting that while S-Corporations offer many benefits, they also require more formality and compliance measures compared to other business structures. S-Corporations must file an annual tax return, adopt bylaws, issue stock, hold regular meetings of the board of directors and shareholders, and keep minutes of all meetings [1].

Having an understanding of the unique structure and features of an S-Corporation will better equip you to navigate the specific challenges and opportunities, particularly when it comes to handling payroll taxes.

S-Corporation Tax Basics

Now that we’ve laid out what an S-Corporation is and how it differs from other business entities, it’s time to go deeper into the specifics of S-Corporation taxation. These tax principles are foundational for understanding how payroll taxes come into play for S-Corporation owners.

Explanation of Pass-Through Taxation

The hallmark of S-Corporation taxation lies in its pass-through nature. But what does “pass-through” taxation mean?

Simply put, pass-through taxation allows the profits (or losses) of the S-Corporation to “pass-through” directly to the shareholders. Instead of the corporation paying federal corporate taxes, the business income is reported on the individual tax returns of the shareholders, and tax is paid at the individual income tax rates. This ability to avoid double taxation is one of the primary reasons why many business owners elect for S-Corporation status.

Benefits of S-Corporation Status for Tax Purposes

The primary tax advantage of an S-Corporation is the avoidance of double taxation, which is a significant relief compared to the C-Corporation structure.

Moreover, S-Corporation shareholders can be employees of the business and draw salaries as employees. They can also receive dividends from the corporation, which could potentially be taxed at a lower rate than ordinary income [2].

Another significant benefit is that S-Corporation shareholders can deduct 100% of their health insurance premiums paid by the S-Corporation, as long as certain conditions are met.

S-Corporation Tax Reporting Requirements

While the tax benefits of an S-Corporation are appealing, it’s crucial to understand the reporting requirements that come with them.

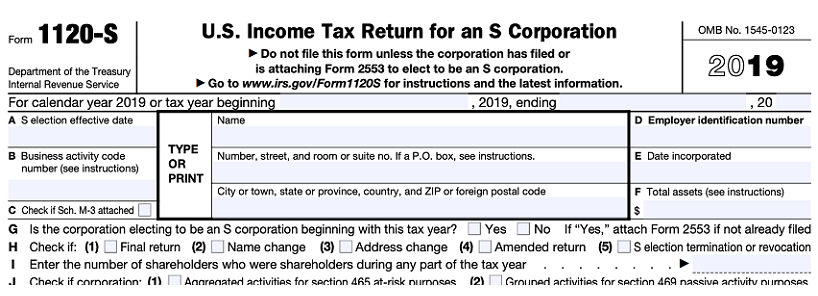

Every year, an S-Corporation must file Form 1120S to report its annual income, deductions, and other important financial information. This form also includes a Schedule K-1 for each shareholder, outlining their share of the corporation’s profits, losses, deductions, and credits. Shareholders must then report this information on their individual tax returns.

Even though S-Corporations avoid corporate-level taxes, they still need to fulfill these tax reporting obligations. Compliance is key to maintaining your S-Corporation status and enjoying its benefits, particularly when it comes to managing payroll taxes.

Payroll Taxes in General

Before we examine how payroll taxes specifically impact S-Corporation owners, let’s start with a general understanding of payroll taxes. Payroll taxes are a critical part of tax compliance for any business with employees, regardless of its structure.

Definition of Payroll Taxes

Payroll taxes are taxes that employers withhold from an employee’s salary and pay directly to the government. These taxes are based on the wage or salary of the employee, and they are used to fund various programs such as Social Security, Medicare, unemployment compensation, and workers’ compensation.

Types of Payroll Taxes and Their Rates

Payroll taxes include two primary types: Social Security tax and Medicare tax. These are also known as Federal Insurance Contributions Act (FICA) taxes.

As of my knowledge cutoff in September 2021, the Social Security tax rate is 6.2% for the employer and 6.2% for the employee, up to the maximum taxable earnings. The Medicare tax rate is 1.45% each for both the employer and the employee, with no income limit. Additionally, there is an extra 0.9% Medicare tax that applies to individuals with earnings above a certain threshold.

Besides FICA taxes, employers also pay Federal Unemployment Tax Act (FUTA) taxes and state unemployment taxes, the rates for which can vary.

Employer’s Responsibility for Payroll Taxes

As an employer, you have several responsibilities concerning payroll taxes. First, you need to withhold the correct amount of payroll tax from your employees’ wages. Second, you must deposit these withheld taxes timely with the IRS. Lastly, you’re required to report these taxes by filing the appropriate forms with the government.

Failing to fulfill these responsibilities can result in hefty penalties, making payroll tax compliance a critical aspect of running your business, especially if you’re an S-Corporation owner [3].

Payroll Taxes for S-Corporation Owners

Now that we’ve covered the fundamentals of payroll taxes, it’s time to understand how these apply to S-Corporations. For S-Corporation owners who also work as employees in their business, payroll taxes have some unique implications.

Distinct Features of Payroll Taxes for S-Corporation Owners

One of the most significant aspects of payroll taxes for S-Corporation owners is that they apply to an owner-employee’s salary but not to distributions or dividends that the owner might receive from the business. This characteristic sets the stage for some strategic tax planning opportunities but also introduces potential complications.

“Reasonable Compensation” for S-Corporation Owners

The IRS requires that S-Corporation owner-employees pay themselves “reasonable compensation” before taking distributions from profits. This reasonable compensation is subject to payroll taxes.

While there isn’t a clear-cut definition of what constitutes “reasonable,” it generally means a salary that’s comparable to what other businesses would pay for similar services. If the IRS finds that an S-Corporation owner isn’t paying a reasonable salary, they could reclassify distributions as wages, leading to additional tax and penalties.

Impact of FICA Taxes on S-Corporations

As we mentioned earlier, FICA taxes consist of Social Security and Medicare taxes. For S-Corporation owners, only the wages they pay themselves as employees are subject to these taxes. Earnings distributed as dividends are not subject to FICA taxes, which can result in substantial tax savings [4].

However, this doesn’t mean you can avoid FICA taxes entirely by not taking any salary. Remember the rule about “reasonable compensation.” You must pay yourself a reasonable salary, which will be subject to FICA taxes, before you can take distributions from the business.

Understanding these unique aspects of payroll taxes for S-Corporation owners can help you plan strategically and avoid unexpected tax liabilities.

Tax Saving Strategies for S-Corporations

Running an S-Corporation opens up several opportunities for tax planning. By understanding these strategies, you can optimize your business finances and potentially save significant amounts on your taxes.

Salary and Dividend Distribution Balance

The most notable tax-saving strategy for S-Corporation owners involves balancing your salary with dividend distributions. Because payroll taxes only apply to your salary and not to distributions, you may be tempted to minimize your salary and take most of your income as dividends.

However, as mentioned before, the IRS requires that you pay yourself a “reasonable salary” before you take distributions. Failing to do so could lead to penalties. Therefore, a careful balance must be struck – you should set your salary at a reasonable level comparable to industry standards, and then take the remaining income as dividends, thereby minimizing your payroll tax liability [5].

Use of Fringe Benefits

Another tax-saving strategy involves fringe benefits. Certain benefits provided by an S-Corporation to its employees can be written off as business expenses, providing a tax-saving opportunity. These may include health insurance premiums, retirement plan contributions, and certain types of employee reimbursement programs.

However, note that the rules around fringe benefits can be complex, and not all benefits are tax-free for all employees. For example, certain benefits may be taxable for shareholder-employees who own more than 2% of the business. Always consult a tax professional when it comes to implementing these strategies.

Retirement Contributions and Tax Savings

Retirement contributions represent another tax-saving strategy. An S-Corporation can establish a retirement plan such as a Simplified Employee Pension (SEP) plan, a Savings Incentive Match Plan for Employees (SIMPLE), or a 401(k). Contributions made to these plans by the S-Corporation on behalf of its employees (including owner-employees) are typically tax-deductible for the business, and they grow tax-free until retirement.

These strategies highlight the potential tax advantages that come with operating as an S-Corporation. By being aware of these, and implementing them in consultation with a tax professional, you can optimize your tax situation and realize significant savings.

References

[1] S Corp and Self Employment Tax: What you need to know

[2] S Corporations and Salaries: An IRS Hot Button Issue

[3] The Dual Tax Burden of S Corporations

[4] S Corporation Profits or Payday

[5] 5 Steps for Filing S Corporation Taxes