In the vast landscape of business entities, the S-Corporation stands out as a unique option for many entrepreneurs and business owners. Offering a blend of tax benefits, liability protection, and operational flexibility, it’s no wonder that many are drawn to its allure. But, diving into the world of S-Corporations isn’t as simple as merely declaring it; a formal election with the Internal Revenue Service (IRS) is crucial.

Introduction to S-Corporation Election

An S-Corporation, often referred to as an “S-Corp,” is a type of business entity that combines the legal protection of a corporation with the tax benefits of a partnership or sole proprietorship. Unlike a traditional C-Corporation, which is taxed at the corporate level and then again at the individual shareholder level, an S-Corp allows profits (and some losses) to be passed directly to the shareholders without being taxed at the corporate level.

The election to become an S-Corporation is not automatic. A business must meet specific requirements and file the appropriate paperwork with the IRS to gain this status. This election can significantly impact the way the business is taxed and how profits and losses flow through to the shareholders. By understanding this process, business owners can make informed decisions about whether the S-Corporation structure is right for their venture and how to maintain the benefits it offers.

Background on the S-Corporation Concept

The world of business structures can be labyrinthine, with each type of entity offering its own set of benefits and drawbacks. To appreciate the unique nature of the S-Corporation, it’s essential to dive into its origins, characteristics, and the distinct differences that set it apart from other business entities.

S-Corporation Definition and Characteristics

At its core, an S-Corporation is a unique tax designation granted by the IRS. The ‘S’ in S-Corporation stands for ‘Subchapter S,’ a reference to a specific section of the Internal Revenue Code. When a business chooses to become an S-Corp, it is essentially opting for a special tax status that allows it to bypass the typical double taxation faced by traditional C-Corporations.

Some defining characteristics of S-Corporations include the following.

Limited Liability Protection

Like other corporate structures, the shareholders’ personal assets are typically protected from business liabilities.

Pass-Through Taxation

Rather than paying taxes at the corporate level, income, and losses are passed through to shareholders and reported on individual tax returns [1].

Restrictions on Ownership

There are limits regarding who can be an S-Corp shareholder and the maximum number of shareholders allowed.

Single Stock Class: S-Corporations are limited to one class of stock, though there can be differences in voting rights.

Differences Between S-Corporations and Other Business Entities

When navigating the business world, it’s imperative to distinguish between the various structures available. Here’s a breakdown of how S-Corporations compare to other common entities.

S-Corp vs. C-Corp

While both entities offer limited liability protection, the primary difference lies in taxation. C-Corporations face double taxation, where the corporation pays taxes on profits, and then shareholders pay taxes on dividends. In contrast, S-Corps benefit from pass-through taxation, avoiding the corporate-level tax.

S-Corp vs. LLC

Limited Liability Companies (LLCs) also enjoy pass-through taxation. However, LLCs offer more flexibility in management structure and profit distribution. Unlike S-Corps, there are no restrictions on the number or type of LLC members.

S-Corp vs. Sole Proprietorship

A sole proprietorship is the simplest business form, owned by a single individual. While it benefits from pass-through taxation, it does not offer the personal asset protection inherent in the S-Corporation structure [2].

Benefits of Electing S-Corporation Status

The appeal of the S-Corporation often lies in the myriad of benefits it offers to business owners. While it’s not a one-size-fits-all solution, for many businesses, the advantages of electing this status can lead to significant operational, financial, and strategic gains.

Taxation Advantages

Undoubtedly, one of the primary motivations behind the S-Corp election is the unique tax treatment it offers.

Pass-Through Taxation

Unlike traditional C-Corporations that face taxation at both the corporate and individual levels, S-Corporations benefit from pass-through taxation. This means the corporation itself doesn’t pay income taxes. Instead, the company’s profits or losses are passed directly to the shareholders, who report this income on their individual tax returns. By bypassing corporate-level taxation, businesses can often achieve significant tax savings.

Avoidance of Double Taxation

Double taxation is a concern for C-Corporations, where profits are taxed at the corporate level and then again when distributed as dividends to shareholders. With the S-Corp structure, profits are only taxed once – at the individual shareholder’s tax rate. This can result in substantial savings, especially for businesses that generate high profits [3].

One of the foundational benefits of any corporate structure is the protection it offers to its owners. S-Corporations are no exception.

Asset Protection

Shareholders of an S-Corp enjoy limited liability protection, meaning their personal assets (like their homes, cars, and personal savings) are typically shielded from any business debts or legal judgments against the corporation. This protection ensures that shareholders can operate with peace of mind, knowing their personal financial wellbeing is safeguarded.

Flexibility in Income Allocation

Income flexibility is a unique advantage for those in the S-Corp structure. While there are regulations to follow, S-Corporations provide certain leeways.

Salary and Dividend Distribution

Owners who work in the business can take a portion of their income as salary and the remaining as dividends. This can lead to potential savings on self-employment taxes, as only the salary portion is subject to these taxes. It’s worth noting, however, that the IRS requires the salary to be “reasonable” for the work performed.

Credibility with Clients and Partners

Often overlooked but equally important is the enhanced credibility that comes with an S-Corporation status.

Professional Image

Incorporating, even as an S-Corp, can provide a boost to a business’s professional image. Clients, suppliers, and partners may view the business as more established and reliable, potentially leading to increased opportunities and collaborations [4].

Process of Electing S-Corporation Status with the IRS

The decision to become an S-Corporation is merely the first step. Bringing this decision to fruition involves a specific process with the Internal Revenue Service (IRS). As with any legal or financial endeavor, understanding the steps, requirements, and potential pitfalls is critical.

Eligibility Requirements

Before diving into the paperwork, it’s essential to determine if your business qualifies for S-Corporation status. The IRS has established specific criteria that a company must meet.

An S-Corp can have no more than 100 shareholders. For the purpose of this rule, families can often be treated as a single shareholder.

Shareholders must be U.S. citizens or resident aliens. Partnerships, other corporations, and non-resident aliens cannot be shareholders.

Classes of Stock

The S-Corp can only have one class of stock. While there can be differences in voting rights associated with the stock, there cannot be differences in distribution rights [5].

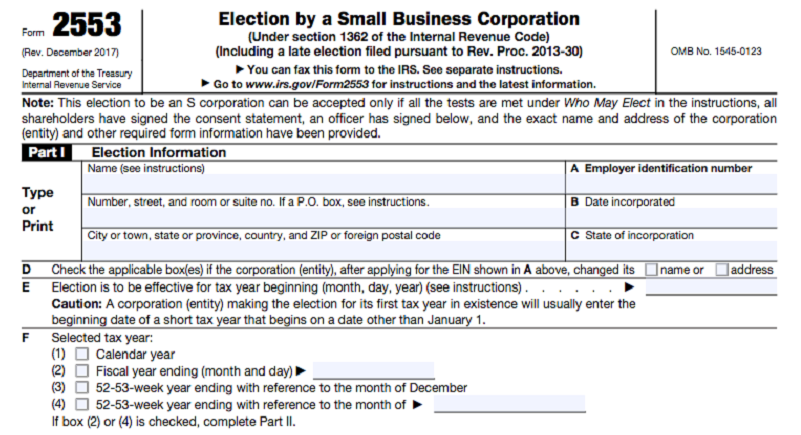

Filing the IRS Form 2553

Once you’ve confirmed your business’s eligibility, the next step is to officially request S-Corporation status by filing Form 2553 with the IRS:

Important Deadlines

To ensure the S-Corporation status applies for the current tax year, you’ll need to file Form 2553:

- No more than two months and 15 days after the beginning of the tax year the election is to take effect, or

- At any time during the tax year preceding the tax year it is to take effect.

Key Sections to Focus On

While each part of Form 2553 is crucial, be especially attentive to:

- Part I, which confirms eligibility.

- Part II, which details the information about the corporation.

- The consent statement section, ensuring all shareholders are in agreement.

Common Mistakes to Avoid

When filling out Form 2553, be wary of:

- Overlooking any shareholder’s consent.

- Missing the filing deadline.

- Providing incomplete or incorrect information.

State-Specific Requirements and Considerations

While the S-Corporation status deals primarily with federal taxation, it’s vital to be aware of state-specific rules and regulations.

State Recognition

Not all states recognize the federal S-Corporation election, and some might tax an S-Corp like a regular corporation. Ensure you’re aware of how your state treats S-Corporations.

Additional Paperwork

Some states require an additional form or a separate state-level S-Corporation election.

Ongoing Requirements

Beyond the initial election, certain states might have unique ongoing requirements for S-Corporations, such as annual reports or minimum taxes.

References

[1] What is an S Corp Election? A Guide for Small Businesses

[2] About Form 2553, Election by a Small Business Corporation

[3] S Corporation Election: Everything You Need to Know

[4] S Corporation Status is Elected on Form 2553

[5] How to Obtain a Copy of a Filed Sub S Corp Election