In the world of business, S-Corporations (S-Corps) stand out as a popular choice for small and medium-sized enterprises seeking the benefits of limited liability and pass-through taxation. However, the road to success for S-Corporations is not without its challenges. One of the key factors influencing the growth and evolution of an S-Corp is the often-overlooked issue of shareholder limitations. Here we examine the intricate web of regulations, qualifications, and restrictions that define shareholder limitations within S-Corporations. By exploring the impact of these limitations, we aim to shed light on the crucial interplay between corporate structure and growth potential.

Contents

Starting and managing a small business can be an exhilarating endeavor, filled with endless possibilities and the promise of growth. When it comes to selecting the right business structure, many entrepreneurs opt for the S-Corporation, or S-Corp, for its appealing blend of limited liability protection and pass-through taxation. This choice often proves advantageous, allowing business owners to protect their personal assets while enjoying tax benefits.

Definition of S-Corporation

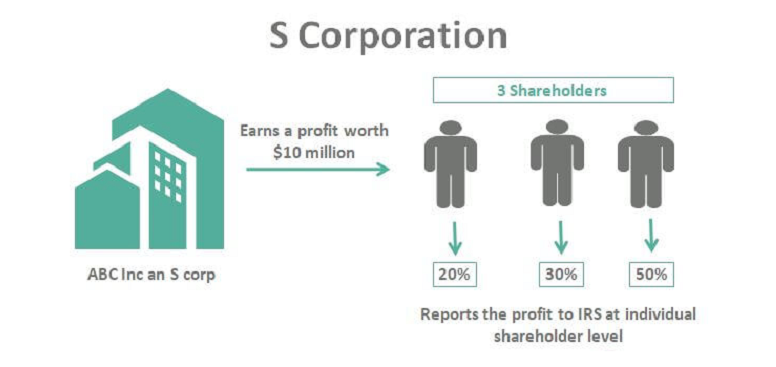

An S-Corporation, or S-Corp for short, is a distinct legal structure that combines the liability protection of a corporation with the tax advantages of a partnership. In simple terms, it’s a business entity that allows its owners, also known as shareholders, to pass business profits and losses directly through their personal tax returns. This means that the S-Corporation itself is not subject to federal income tax. Instead, shareholders report their share of the company’s income or losses on their individual tax returns, which can lead to potential tax savings.

While the S-Corporation structure offers numerous benefits, it’s essential to recognize that it comes with specific limitations, particularly regarding its shareholders. These limitations are not just legal formalities; they can profoundly affect the way the company operates and grows. Understanding these limitations is crucial for business owners considering or currently operating as an S-Corp.

Preview of the Impact on S-Corporation Growth

Shareholder limitations encompass qualifications, restrictions, and regulations governing who can invest in an S-Corp, how many shareholders are allowed, and the types of entities that can hold shares. These limitations can influence various aspects of an S-Corporation’s journey, from attracting investment to governance and tax benefits.

Now that we have a solid understanding of what an S-Corporation is and why it’s an attractive choice for business owners, let’s delve into the heart of the matter: the complexities of shareholder limitations within the S-Corp structure. These limitations are not merely formalities but play a pivotal role in how an S-Corporation functions and evolves.

To maintain S-Corporation status, it’s crucial to ensure that shareholders meet certain eligibility criteria. Typically, individual U.S. citizens or residents, estates, and certain trusts are eligible shareholders. Corporations and partnerships, for instance, cannot hold shares in an S-Corp [1].

Another critical limitation relates to the number of shareholders. S-Corps are restricted to a maximum of 100 shareholders. This limit can impact the company’s ability to raise capital and its overall ownership structure.

Individuals

Individual shareholders are the most common in S-Corporations. They include business founders, employees, and other individuals who invest in the company.

Trusts

Certain types of trusts, such as grantor trusts, can be eligible S-Corporation shareholders. However, it’s essential to understand the specific rules governing trust ownership in S-Corps.

Estates

Estates of deceased individuals can hold S-Corporation shares. This provision allows for the orderly transfer of ownership upon the passing of a shareholder.

Certain Organizations

While most business entities cannot be S-Corporation shareholders, certain tax-exempt organizations, such as 501(c)(3) organizations, can hold shares [2].

S-Corporations often issue different classes of shares with varying rights and privileges. However, all classes must have identical economic rights to ensure pass-through taxation.

Voting Rights Limitations

Shareholder agreements and corporate bylaws can impose voting rights limitations. For instance, some shares may have voting rights while others may not, leading to disparities in corporate governance.

Shareholder limitations aren’t just regulatory hurdles; they can significantly impact various aspects of an S-Corporation’s growth and operation.

Impact on Capital Investment

Limited Ability to Attract Investors

The 100-shareholder limit can be a double-edged sword. While it fosters a sense of exclusivity, it can also hinder an S-Corp’s ability to attract a diverse pool of investors. This limitation can be especially challenging for businesses seeking substantial capital infusions for expansion.

Raising Capital Challenges

S-Corporations may face difficulties in raising capital compared to their C-Corporation counterparts. The limitations on the types of shareholders and the number of shareholders can deter potential investors, potentially slowing down growth initiatives [3].

Governance and Decision-Making

Board of Directors Composition

The composition of the board of directors in an S-Corporation can be influenced by shareholder limitations. With fewer shareholders and varying voting rights, control over the board’s composition may become a contentious issue.

In smaller S-Corporations, a single major shareholder or a few dominant shareholders can wield significant influence over key decisions. This concentration of power can impact the company’s strategic direction and decision-making processes.

Tax Benefits and Compliance

Maintaining S-Corporation Status

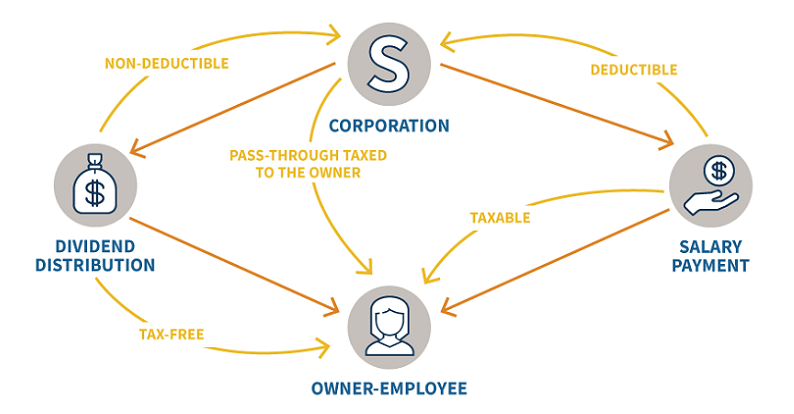

Shareholder limitations are closely tied to S-Corporation tax benefits, including pass-through taxation. Failing to meet these limitations can result in the loss of S-Corp status and a shift to less favorable tax treatment, such as that of a C-Corporation.

Pass-Through Taxation Benefits

Shareholder limitations play a pivotal role in preserving pass-through taxation benefits, allowing profits and losses to flow through to individual shareholders. This tax advantage can be a significant driver of S-Corporation growth [4].

While S-Corporation shareholder limitations are inherent to the structure, there are strategic approaches that savvy business owners can employ to navigate these restrictions effectively.

Buy-Sell Agreements

Implementing buy-sell agreements can provide a structured way to address changes in ownership. These agreements allow shareholders to buy or sell their shares under specific circumstances, such as retirement, death, or the desire to exit the company. By including buy-sell provisions in your corporate documents, you can maintain control over who becomes a shareholder.

Voting Agreements

Voting agreements can help regulate decision-making processes by defining how voting rights are exercised among shareholders. This can be particularly useful in situations where there are different classes of shares with varying voting powers.

Exploring Alternative Business Structures

Comparing S-Corporations to Other Entities

It’s essential to periodically evaluate whether the S-Corporation structure is the best fit for your business. Depending on your growth plans and shareholder limitations, you may find that another business entity, such as a Limited Liability Company (LLC) or a C-Corporation, better suits your needs [5].

Conversion to a C-Corporation

If your business has outgrown the limitations of an S-Corporation, you might consider converting to a C-Corporation. This allows for an unlimited number of shareholders and diverse ownership structures, although it comes with different tax implications.

Diversifying Sources of Capital

Exploring Debt Financing

To overcome the challenges of limited equity investment, consider exploring debt financing options. Loans, lines of credit, and business credit cards can provide essential capital for growth without diluting ownership.

Crowdfunding and Alternative Funding Options

In the digital age, crowdfunding and alternative funding platforms have become popular ways to raise capital. These options can enable you to access a broader pool of potential investors and supporters.

References

[1] S Corporation stock and debt basis

[2] s corporation shareholder limit

[3] Managing S Corporation At-Risk Loss Limitations

[4] Limiting Your Liability with LLCs and S Corporations

[5] Tax-Option (S) Corporation Shareholder Reporting Questions